How New Structural Materials Could Redefine the Economics of Decarbonising the Built Environment

新型结构材料如何重新定义建筑环境脱碳的经济逻辑

Introduction: Why the Built Environment Is Entering a New Decarbonisation Phase

The global building and construction sector remains one of the largest contributors to climate change, accounting for approximately 37% of global energy-related CO₂ emissions. Over the past decade, most decarbonisation efforts have focused on reducing operational emissions — through energy efficiency, electrification, and renewable energy integration.

Yet a structural challenge remains largely unresolved: embodied carbon — the emissions generated by producing, transporting, and assembling construction materials such as cement, steel, and conventional concrete. As buildings become more energy-efficient in use, embodied carbon is increasingly becoming the dominant source of emissions over a building’s lifecycle.

A new technological frontier is now emerging: carbon-negative construction materials. These materials do not merely reduce emissions — they actively absorb and permanently store CO₂, transforming buildings from carbon liabilities into potential climate-positive assets.

For businesses, investors, and policymakers, this shift represents not just a sustainability innovation, but a fundamental change in how construction materials are valued, regulated, and financed.

引言:为何建筑环境正在进入新的脱碳阶段

全球建筑与施工行业仍然是气候变化的最大贡献来源之一,约占全球能源相关二氧化碳排放的 37%。在过去十年中,大多数脱碳努力主要集中于减少运营阶段排放——通过提升能源效率、电气化以及可再生能源的整合。

然而,一个结构性挑战在很大程度上仍未解决:隐含碳(embodied carbon)——即在生产、运输和组装水泥、钢铁和传统混凝土等建筑材料过程中产生的排放。随着建筑在使用阶段变得越来越节能,隐含碳正日益成为建筑全生命周期中占主导地位的排放来源。

一个新的技术前沿正在显现:负碳建筑材料。这类材料不仅仅是减少排放——它们能够主动吸收并永久储存二氧化碳,将建筑从碳负担转变为潜在的气候正效建筑。

对于企业、投资者和政策制定者而言,这一转变不仅代表着一项可持续创新,更意味着建筑材料在价值评估、监管方式和融资逻辑上的根本性变化。

What Are Carbon-Negative Construction Materials?

Carbon-negative construction materials are designed to remove more carbon dioxide from the atmosphere than they emit across their full lifecycle. Unlike traditional “low-carbon” solutions, their climate value is based on net carbon removal, not only emission avoidance.

Recent innovation pathways include:

- Carbon mineralisation, where captured CO₂ is converted into stable mineral compounds embedded in building materials.

- Bio-based and enzyme-enabled processes, which accelerate CO₂ conversion into solid structural components.

- Hybrid systems, combining engineered timber, mineral binders, and advanced curing techniques.

A notable recent breakthrough involves enzymatic structural materials, in which biological catalysts rapidly convert CO₂ into mineralised solids during material formation. These materials aim to match the mechanical performance of conventional concrete while delivering net-negative embodied emissions.

Although still at an early commercial stage, these innovations signal a shift from incremental efficiency improvements toward materials that directly contribute to climate mitigation.

什么是负碳建筑材料?

负碳建筑材料的设计目标,是在其完整生命周期内从大气中移除的二氧化碳多于其自身排放量。不同于传统的“低碳”解决方案,其气候价值基于净碳移除,而不仅仅是避免排放。

近期的创新路径包括:

- 碳矿化,即将捕集的二氧化碳转化为稳定的矿物化合物,并嵌入建筑材料中。

- 生物基和酶促过程,加速二氧化碳向固体结构组分的转化。

- 混合系统,结合工程木材、矿物胶结材料和先进养护技术。

近期一个引人注目的突破涉及酶促结构材料,其中生物催化剂在材料成型过程中快速将二氧化碳转化为矿化固体。这类材料旨在在实现与传统混凝土相当的力学性能的同时,实现隐含排放的净负值。

尽管仍处于早期商业化阶段,这些创新清晰地表明,建筑材料正在从渐进式效率提升,转向直接为气候减缓作出贡献的路径。

Why Carbon-Negative Materials Matter for Business?

From Compliance Cost to Strategic Value

Traditionally, decarbonisation in construction has been viewed as a cost driver — higher material prices, compliance investments, and reporting obligations. Carbon-negative materials introduce a new economic logic.

By storing CO₂ within buildings, they create the potential for:

- Embodied carbon monetisation through voluntary or regulated carbon markets

- Improved eligibility for green finance and sustainability-linked loans

- Stronger ESG performance at asset and portfolio level

In carbon-constrained markets, carbon performance increasingly translates into financial value.

Regulatory Momentum Is Accelerating

Regulatory frameworks are moving rapidly toward lifecycle carbon control:

- The EU Energy Performance of Buildings Directive (EPBD) increasingly addresses whole-life carbon emissions

- Several EU member states are introducing mandatory embodied-carbon reporting for new developments

- Green public procurement rules prioritise low- and zero-carbon materials

Carbon-negative materials offer developers and suppliers a way to anticipate regulation rather than react to it, reducing long-term compliance risk.

Real Estate Valuation and Investor Expectations

Institutional investors are now assessing assets based on:

- Long-term transition risk

- Regulatory exposure

- Alignment with net-zero pathways

Buildings incorporating carbon-negative materials can:

- Improve asset resilience under tightening climate policy

- Enhance eligibility for EU taxonomy-aligned investments

- Support higher long-term valuation stability

Material choice at construction stage is becoming a strategic financial decision, not a purely technical one.

为何负碳材料对企业至关重要?

从合规成本到战略价值

传统上,建筑领域的脱碳往往被视为成本驱动因素——更高的材料价格、合规投入以及报告义务。负碳材料则引入了一种新的经济逻辑。

通过在建筑中储存二氧化碳,它们创造了以下潜在价值:

- 通过自愿或受监管的碳市场实现隐含碳的货币化

- 提升获得绿色金融和可持续挂钩贷款的资格

- 在资产和投资组合层面强化 ESG 表现

在碳受限的市场中,碳绩效正日益转化为金融价值。

监管动能正在加速

监管框架正迅速迈向生命周期碳控制:

- 欧盟《建筑能效指令》(EPBD)日益关注全生命周期碳排放

- 若干欧盟成员国正在对新开发项目引入强制性的隐含碳报告要求

- 绿色公共采购规则优先采用低碳和零碳材料

负碳材料为开发商和供应商提供了一种前瞻监管、而非被动应对监管的方式,从而降低长期合规风险。

房地产估值与投资者预期

机构投资者正基于以下因素评估资产:

- 长期转型风险

- 监管暴露程度

- 与净零路径的一致性

采用负碳材料的建筑可以:

- 在紧缩的气候政策下提高资产弹性

- 增强符合欧盟分类法(EU taxonomy)投资的资格

- 支撑更高的长期估值稳定性

在建筑阶段对材料的选择,正逐渐成为一项战略性的金融决策,而不再只是纯技术问题。

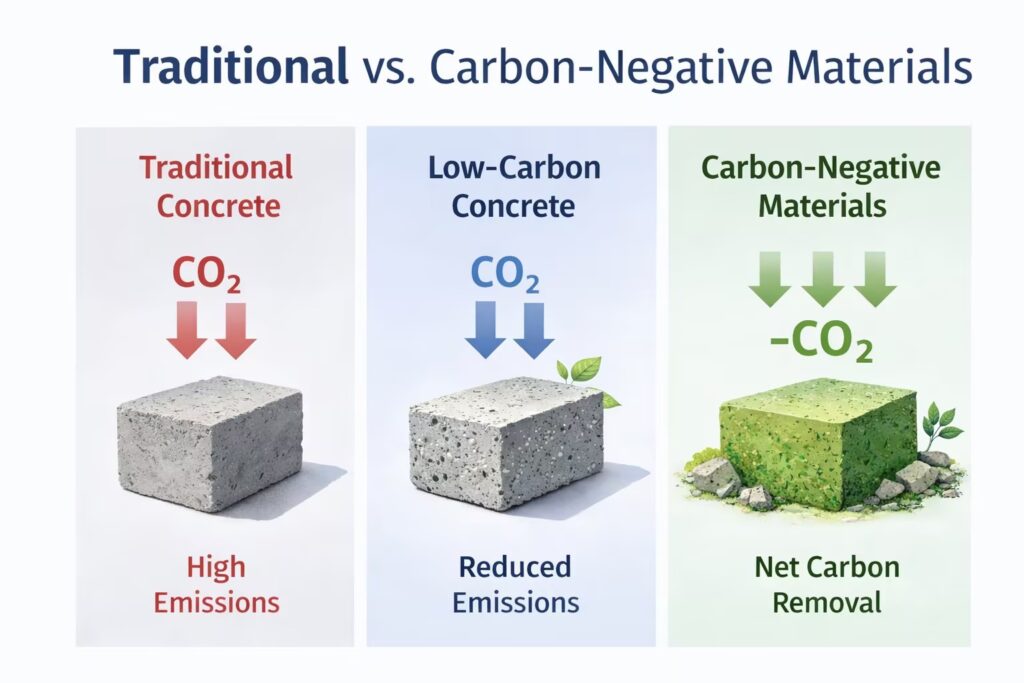

Quantified Comparison: Traditional vs Carbon-Negative Materials

Indicator | Traditional Concrete / Cement | Low-Carbon Concrete | Carbon-Negative Materials |

Embodied CO₂ emissions | ~600–900 kg CO₂ / m³ | ~300–500 kg CO₂ / m³ | –50 to –200 kg CO₂ / m³ |

Carbon performance | High emissions | Reduced emissions | Net carbon removal |

Regulatory readiness | Increasingly exposed | Transitional solution | Future-proof |

Market maturity | Fully mature | Growing | Early commercial stage |

Cost today | Low | Medium | Medium–high (declining) |

Strategic value | Compliance risk | Risk mitigation | Carbon asset potential |

Figures are indicative and vary by technology, location, and lifecycle assumptions.

定量对比:传统材料 vs 负碳材料

指标 | 传统混凝土 / 水泥 | 低碳混凝土 | 负碳材料 |

隐含 CO₂ 排放 | ~600–900 kg CO₂ / m³ | ~300–500 kg CO₂ / m³ | –50 to –200 kg CO₂ / m³ |

碳绩效 | 高排放 | 减排 | 净碳移除 |

监管适配度 | 暴露度不断上升 | 过渡性解决方案 | 面向未来 |

市场成熟度 | 完全成熟 | 成长中 | 早期商业阶段 |

当前成本 | 低 | 中 | 中–高(下降中) |

战略价值 | 合规风险 | 风险缓释 | 碳资产潜力 |

上述数据为示意性数值,具体情况因技术、地区及生命周期假设而异。

China-Specific Policy Signals and Pilot Opportunities

China is progressively creating conditions for advanced low-carbon and carbon-negative materials to move from research to early deployment, particularly within urban regeneration and public construction.

Key policy and market signals include:

- Evolution of Green Building Evaluation Standards (GB/T 50378) toward lifecycle carbon considerations

- Low-carbon city and industrial park pilots, where innovative materials can be tested in public projects

- Large-scale urban renewal programmes, where embodied carbon reduction and material reuse are becoming explicit objectives

Cities such as Shanghai, Shenzhen, Guangzhou, and Beijing are encouraging demonstration projects that integrate innovative low-carbon materials in municipal buildings, schools, and public housing. While most pilots currently focus on recycled aggregates and low-carbon concrete, the policy trajectory clearly opens space for next-generation carbon-negative materials, particularly when linked to innovation incentives or green finance mechanisms.

For international material developers, China offers opportunities through:

- Joint pilot projects with local governments

- Licensing and co-development with major construction groups

- Integration into low-carbon city frameworks

中国相关的政策信号与试点机遇

中国正逐步为先进的低碳与负碳材料从研究走向早期应用创造条件,尤其是在城市更新和公共建设领域。

关键政策与市场信号包括:

- 《绿色建筑评价标准》(GB/T 50378)向生命周期碳考量方向演进

- 低碳城市与产业园区试点,为创新材料在公共项目中的测试提供空间

- 大规模城市更新计划,其中隐含碳减排和材料再利用正成为明确目标

上海、深圳、广州和北京等城市正鼓励在市政建筑、学校和公共住房中开展融合创新低碳材料的示范项目。尽管当前大多数试点仍聚焦于再生骨料和低碳混凝土,但政策走向已清晰地为下一代负碳材料打开空间,尤其是在与创新激励或绿色金融机制相结合的情况下。

对于国际材料开发商而言,中国提供了以下机遇:

- 与地方政府开展联合试点项目

- 与大型建筑集团进行许可合作与联合开发

- 纳入低碳城市整体框架

Examples of Emerging Carbon-Negative Construction Materials

Several material families illustrate how carbon-negative construction may evolve:

- Carbon-mineralised concrete alternatives

These materials inject captured CO₂ into cementitious systems, transforming it into stable carbonate minerals. The process not only reduces cement demand but permanently stores carbon, while maintaining structural performance suitable for a wide range of applications.

- Bio-based and enzyme-enabled structural materials

Using biological catalysts, these materials accelerate the conversion of CO₂ into solid mineral components. They are particularly promising for prefabricated elements, façades, and modular construction, combining durability with active carbon sequestration.

- Engineered timber and hybrid systems

When sourced from sustainably managed forests and combined with mineral binders or bio-based resins, advanced timber systems can achieve net-negative embodied carbon, especially in mid-rise residential and commercial buildings.

Together, these technologies show that the construction sector is moving beyond “less carbon” toward materials that actively remove carbon from the atmosphere.

新兴负碳建筑材料的示例

若干材料类别展示了负碳建筑可能的发展方向:

- 碳矿化混凝土替代材料

这些材料将捕集的二氧化碳注入水泥基体系中,将其转化为稳定的碳酸盐矿物。该过程不仅降低了水泥需求,还实现了碳的永久储存,同时保持适用于广泛应用场景的结构性能。

- 生物基与酶促结构材料

通过生物催化剂,这类材料加速二氧化碳向固体矿物组分的转化。它们在预制构件、立面和模块化建筑中尤具潜力,将耐久性与主动碳封存相结合。

- 工程木材与混合系统

当来自可持续管理森林的木材与矿物胶结材料或生物基树脂相结合时,先进的木结构体系可实现隐含碳的净负值,尤其适用于中高层住宅和商业建筑。

这些技术共同表明,建筑行业正从“更少的碳”迈向主动从大气中移除碳的材料体系。

China–EU Complementarity: A Strategic Opportunity

Europe and China bring complementary strengths to the development of carbon-negative construction materials:

- Europe: strong regulatory push, advanced material research, growing demand for climate-positive buildings

- China: unmatched construction scale, rapid industrialisation capacity, increasing policy support for green buildings

This creates a natural basis for:

- Joint R&D and pilot projects

- Technology transfer and standard development

- Cross-border investment in sustainable construction value chains

For companies operating across both markets, carbon-negative materials can become a strategic bridge between innovation leadership and large-scale deployment.

中欧互补性:一项战略机遇

欧洲与中国在负碳建筑材料的发展方面具备互补优势:

- 欧洲: 强有力的监管推动、先进的材料研究、对气候正建筑不断增长的需求

- 中国: 无可匹敌的建设规模、快速的产业化能力、对绿色建筑日益增强的政策支持

这为以下合作奠定了天然基础:

- 联合研发与试点项目

- 技术转移与标准制定

- 可持续建筑价值链中的跨境投资

对于同时在两大市场运营的企业而言,负碳材料可以成为连接创新领先与规模化部署的战略桥梁。

Challenges That Still Need to Be Addressed

Despite strong momentum, several barriers remain:

- Cost competitiveness versus conventional materials

- Standardisation and certification of safety and performance

- Supply-chain readiness for industrial-scale deployment

- Market education among developers, contractors, and regulators

Overcoming these challenges will require coordinated action across the value chain, supported by policy clarity and financial incentives.

仍需应对的挑战

尽管势头强劲,仍存在若干障碍:

- 与传统材料相比的成本竞争力

- 安全性与性能的标准化与认证

- 面向工业化规模部署的供应链准备度

- 开发商、承包商与监管机构的市场认知

克服这些挑战,需要在清晰政策指引和金融激励支持下,整个价值链的协同行动。

Conclusion: From Experimental Materials to Strategic Assets

Carbon-negative construction materials represent a structural shift in how buildings are conceived — not merely as energy-efficient objects, but as active contributors to climate mitigation.

For businesses, the implications are profound:

- Material innovation becomes a competitive differentiator

- Carbon performance evolves into a financial and regulatory asset

- Buildings transform into long-term climate-positive infrastructure

As China and Europe accelerate their decarbonisation agendas, carbon-negative materials stand out as a tangible example of how technology, policy, and market forces can align to reshape an entire sector.

The key strategic question is no longer whether these materials will enter the mainstream — but how early companies choose to integrate them into their long-term development, investment, and partnership strategies.

结论:从实验性材料到战略资产

负碳建筑材料代表了建筑理念上的一次结构性转变——建筑不再仅仅被视为高能效对象,而是成为主动参与气候减缓的组成部分。

对企业而言,其影响深远:

- 材料创新成为竞争差异化因素

- 碳绩效演变为金融与监管资产

- 建筑转化为长期的气候正效建筑

随着中国和欧洲加速推进脱碳议程,负碳材料成为技术、政策与市场力量协同重塑整个行业的一个切实例证。

关键的战略问题已不再是这些材料是否会进入主流——而在于企业将多早把它们纳入自身的长期发展、投资与合作战略之中。