Unlocking Recovery Through Policy-Driven Transformation and International Synergies

通过政策驱动的转型和国际化来开启复苏进程

A Sector in Transition

China’s real estate sector, once a cornerstone of its economic growth, is facing a prolonged downturn that poses significant challenges for the broader economy.

With residential sales weakening, commercial space oversupplied, and industrial parks underutilized in certain regions, restoring confidence in the market is more critical than ever. However, this crisis also brings a unique opportunity: to reshape the industry into a greener, more sustainable and innovation-driven force.

At the heart of this effort lies the potential for strengthened collaboration between China and Europe. The EU’s advanced experience in sustainable urban regeneration, combined with China’s massive domestic market and green transition commitments, forms a powerful foundation for joint success.

处于转型中的房地产行业

中国房地产行业曾是中国经济增长的基石,如今正面临着长期的低迷,这给整体经济带来了重大挑战。

随着住宅销售疲软、商业空间供过于求,以及某些地区的工业园区未得到充分利用,恢复市场信心比以往任何时候都更加关键。然而,这场危机也带来了一个独特的机遇:将该行业重塑为一支更绿色、更具可持续性且以创新驱动的力量。

这项努力的核心在于中国和欧洲之间加强合作的潜力。欧盟在可持续城市更新方面的先进经验,与中国庞大的国内市场以及绿色转型的承诺相结合,为双方的共同成功奠定了坚实的基础。

Property Market: Current Landscape and Trends

– Residential Property Market: Current Landscape and Trends

The Chinese residential property market continues to face downward pressure. According to data from the National Bureau of Statistics, new home prices in 70 major cities dropped by 0.3% month-on-month in April 2025. Tier-1 cities such as Beijing and Shanghai remain more resilient due to strong demand, but Tier-2 and Tier-3 cities are seeing significant price declines and inventory overhangs. Developers are struggling with liquidity, and consumer confidence remains low, leading to weak sales.

The central government has rolled out various stimulus measures, including lowering mortgage rates, reducing down payment ratios, and promoting urban redevelopment, but these have had only modest short-term impact. To sustain recovery, deeper reforms and new models of development are needed.

Walking through Shanghai’s Lujiazui financial district, cranes still dot the skyline as luxury developments continue attracting buyers. Meanwhile, in smaller cities like Langfang, entire blocks of vacant apartments stand as silent reminders of the market’s growing divide.

The Numbers Tell the Tale:

– Tier 1 cities (Shanghai, Beijing, Shenzhen) have seen modest 1-3% price growth, supported by:

o Steady demand from high-net-worth buyers

o Government stabilization measures

o Limited new supply in prime locations

– But venture into Tier 2-3 markets, and the picture changes dramatically:

o Zhengzhou and Tianjin report 10-15% price declines

o Smaller cities like Yinchuan face 20%+ drops in values

What This Means:

-The era of universal price growth is over since several year and it will not get back anymore. Today’s market rewards:

✓ Locations with strong employment bases

✓ Cities implementing smart urban planning

✓ Developments offering genuine quality-of-life benefits

– Commercial Real Estate Market: Oversupply and Repositioning

The commercial property market in China faces structural issues. Office vacancy rates in key cities like Shenzhen and Wuhan have reached 25% or more (Shenyang almost 30%), fueled by overbuilding and post-pandemic hybrid work trends. Retail space is also oversupplied in many cities, as e-commerce continues to disrupt traditional shopping patterns.

However, emerging trends such as mixed-use developments, green-certified office buildings, and adaptive reuse of commercial spaces show potential. Forward-looking projects increasingly integrate digital infrastructure, energy efficiency, and lifestyle-focused design to attract tenants.

Among some spotlight on success stories, could be mentioned Sino-Ocean Taikoo Li, in Chengdu, which combines retail, dining and cultural spaces to create vibrant 24/7 communities, as well as Hangzhou’s future-facing office parks. It integrates co-working, R&D labs and green spaces to attract tech tenants.

– Industrial Real Estate: Uneven Dynamics

China’s industrial real estate sector is showing a mixed picture. On one hand, demand for logistics and warehousing in coastal and e-commerce-driven regions (such as the Yangtze River Delta and Pearl River Delta) remains strong. On the other hand, industrial parks in inland provinces often suffer from underutilization, outdated facilities, or weak demand.

Green industrial parks, with better integration of renewable energy, low carbon infrastructures and digital systems, are increasingly in demand. Local and foreign industrial investors are targeting nearly carbon zero, well-connected, and sustainable industrial zones as part of global supply chain diversification efforts.

房地产市场:当前格局与趋势

– 住宅房地产市场:当前格局与趋势

中国住宅房地产市场持续面临下行压力。根据国家统计局的数据,2025年4月,70个大中城市的新建住宅价格环比下降了0.3%。北京和上海等一线城市由于需求强劲,仍具有较强的韧性,但二三线城市的房价大幅下跌,库存积压严重。开发商面临着资金流动性问题,消费者信心依然低迷,导致销售疲软。

中央政府已出台了各种刺激措施,包括降低房贷利率、降低首付比例以及推进城市更新改造,但这些措施在短期内仅产生了有限的影响。要实现持续复苏,还需要进行更深入的改革,并探索新的发展模式。

漫步在上海的陆家嘴金融区,天际线上仍可见许多起重机,豪华楼盘持续吸引着购房者。与此同时,在像廊坊这样的小城市,成片的空置公寓无声地提醒着人们市场分化日益加剧。

数据说明一切:

– 一线城市(上海、北京、深圳)的房价在以下因素的支撑下,实现了1%-3%的小幅增长:

o 高净值购房者的稳定需求

o 政府的稳定市场措施

o 黄金地段的新供应有限

– 但进入二三线城市市场,情况则截然不同:

o 郑州和天津的房价下跌了10%-15%

o 像银川这样的小城市,房价跌幅超过20%

这就意味着:

– 房价普遍上涨的时代已经过去好几年了,而且不会再回来了。如今的市场青睐以下地方:

o 就业基础雄厚的地段

o 实施明智城市规划的城市

o 能真正提供生活品质提升的楼盘项目

– 商业房地产市场:供过于求与重新定位

中国的商业房地产市场面临着结构性问题。由于过度建设以及疫情后混合办公模式的兴起,深圳和武汉等重点城市的写字楼空置率已达到25%或更高(沈阳接近30%)。在许多城市,零售空间也供过于求,因为电子商务持续冲击着传统的购物模式。

然而,一些新兴趋势展现出了潜力,如综合用途开发项目、获得绿色认证的写字楼以及商业空间的适应性再利用。具有前瞻性的项目越来越多地整合了数字基础设施、能源效率和以生活方式为核心的设计理念,以吸引租户。

在一些成功案例中,值得一提的是成都的远洋太古里,它将零售、餐饮和文化空间相结合,打造出了充满活力的24/7全天候社区;还有杭州面向未来的办公园区,它融合了联合办公空间、研发实验室和绿地,以吸引科技企业租户。

– 工业房地产:发展态势不均衡

中国的工业房地产领域呈现出复杂多样的局面。一方面,沿海地区以及电子商务发达地区(如长江三角洲和珠江三角洲)对物流和仓储的需求依然强劲。另一方面,内陆省份的工业园区往往存在利用率不足、设施陈旧或需求疲软的问题。

对绿色工业园区的需求正在日益增长,这类园区能更好地整合可再生能源、低碳基础设施和数字系统。作为全球供应链多元化努力的一部分,国内外的工业投资者正瞄准那些近乎零碳排放、交通便利且可持续发展的工业区。

“Good House” Policy: From Vision to Action

The Ministry of Housing and Urban-Rural Development’s “Good House” initiative aims to shift the focus from quantity to quality in China’s residential construction. It’s about building better communities while not more just about building more units. The policy encourages developers to build homes that are safe, durable, energy-efficient, and equipped with smart systems.

Recent implementation measures include mandatory energy efficiency standards, greater emphasis on building envelope performance, incentives for smart home integration, and pilot programs in major cities such as Hangzhou and Chongqing.

These initiatives are gradually transforming market expectations and creating demand for high-quality, sustainable housing. We have also seen 30+ pilot cities offering developer incentives for compliance and a surge in prefabricated construction, which can reduce waste by 15%.

Key Requirements Rolled Out:

– Energy Efficiency Upgrades: New buildings must achieve at least 3-star green certification

– Smart Home Standards: Mandatory IoT systems for safety and energy management

– Human-Centric Design: Minimum living space increased to 25m² per person

“好房子”政策:从愿景到行动

住房和城乡建设部的“好房子”倡议旨在将中国住宅建设的重点从数量转向质量。这不仅关乎建造更多的住宅单元,更在于打造更优质的社区。该政策鼓励开发商建造安全、耐用、节能且配备智能系统的房屋。

近期的实施措施包括强制推行能效标准,更加注重建筑围护结构的性能,出台激励措施推动智能家居集成,以及在杭州、重庆等主要城市开展试点项目。

这些举措正逐渐改变市场预期,并催生了对高品质、可持续住房的需求。我们还看到,有30多个试点城市为遵守规定的开发商提供激励措施,预制建筑的数量大幅增加,这可以减少15%的浪费。

推出的关键要求:

-能效提升:新建建筑必须至少达到绿色建筑三星级认证标准

-智能家居标准:强制安装用于安全和能源管理的物联网系统

-以人为本的设计:人均最低居住面积提高到25平方米

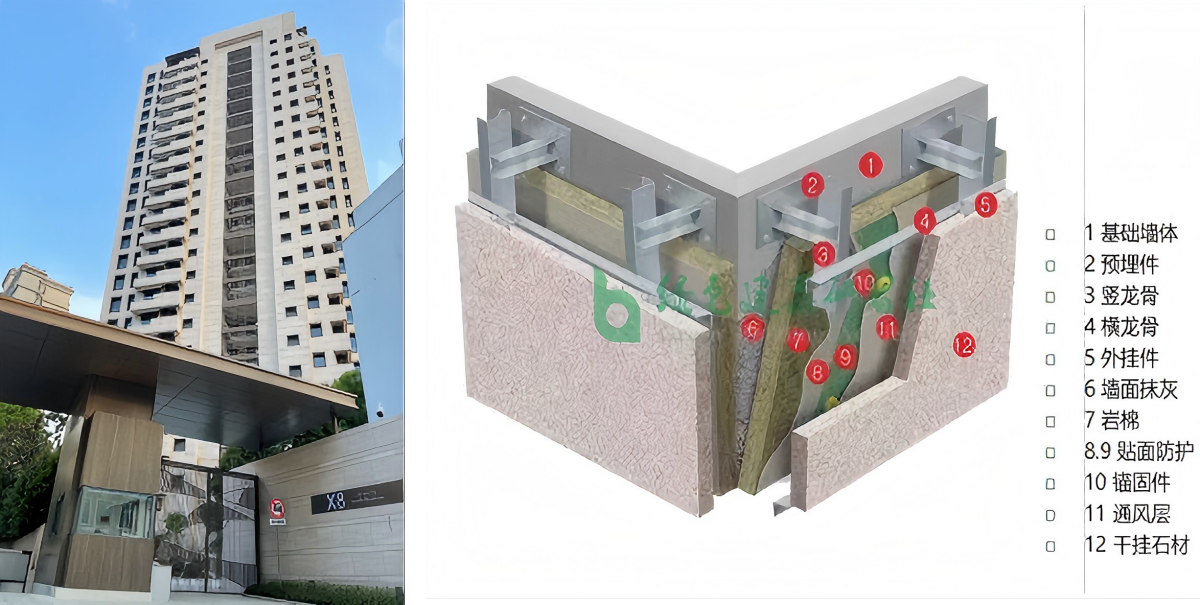

X8 Service Apartment, Shanghai – by Shanghai Urban Construction (Citiraise) Industrial (Group)

上海徐汇X8高端服务式公寓加推3房大户型_知寓服务式公寓网-上海城建建设实业(集团)有限公司

Strategic Proposals for Construction & Real Estate Revitalization

Among the key actions to be taken for a revitalization of the civil construction sector, then the real estate market, CNEUCN and its business partners, identified the followings:

– Green Retrofit Revolution

Inspired by Berlin’s successful renovation strategy, China could launch large-scale retrofitting of aging buildings to achieve net-zero standards. This would support energy savings, job creation, and a new green service industry.

– Next-Gen Construction Techniques

Wider use of prefabricated and passive buildings, as pioneered by Shanghai Urban Construction (Citiraise) Industrial (Group), and cutting-edge methods like 3D printing can dramatically reduce time, cost, and emissions along the production, construction and also building lifecycle, boosting confidence in the quality of new builds.

– Branding of Residential Properties

Assigning iconic brand names to properties helps instill consumer trust and reposition real estate as a lifestyle choice with “certified high-quality”, improved running and ‘lifestyle promise”. This branding strategy can drive demand, particularly in first-home buyers and urban middle-class segments. Italian lifestyle brand Tonino Lamborghini has marked the Chinese market in this regard with successful cases both in hospitality and residential.

– EU Governance Synergies for Sustainable Building

China can benefit from Europe’s extensive regulatory experience, including the Energy Performance of Buildings Directive (EPBD) and renovation wave strategies. Shared approaches to building certification, renovation standards, and incentive mechanisms would not only improve local quality but also enable cross-border recognition and investment.

– Real Estate Investment Trusts (REITs) for Social Good

Singapore’s example shows how REITs can fund affordable, green housing. China can expand its REIT framework to support mixed-income, energy-efficient housing developments, attracting both institutional and retail investors.

– Debt-for-Sustainability Swaps

By linking debt restructuring to sustainability outcomes, developers can gain financial breathing room while committing to green upgrades. This innovative financing model could be piloted in high-priority urban regeneration zones.

建筑与房地产振兴的战略建议

仲欧脱碳科技(CNEUCN)及其商业合作伙伴确定了为振兴民用建筑行业以及房地产市场而需采取的关键行动,具体如下:

– 绿色改造革命

受柏林成功的建筑改造策略启发,中国可以对老旧建筑展开大规模改造,使其达到净零排放标准。这将有助于实现节能目标、创造就业机会,并催生一个新的绿色服务产业。

– 新一代建筑技术

更广泛地采用预制建筑和被动式建筑(如上海城建建设实业(集团)有限公司所开创的范例),以及3D打印等前沿技术,能够大幅减少生产、施工以及建筑生命周期内的时间、成本和排放,提升人们对新建建筑质量的信心。

– 住宅物业品牌化

为房产赋予标志性品牌名称有助于增强消费者的信任,并将房地产重新定位为一种具有 “高品质认证”、完善运营和 “生活方式承诺” 的生活方式选择。这一品牌战略能够拉动需求,尤其是在首次购房者和城市中产阶级群体中。意大利生活方式品牌托尼洛・兰博基尼 (Tonino Lamborghini) 在进军中国市场的过程中,于酒店业和住宅领域均打造出了成功范例。

– 借鉴欧盟治理经验推动可持续建筑发展

中国可以借鉴欧洲丰富的监管经验,包括《建筑能源绩效指令》(EPBD)和建筑改造浪潮战略。在建筑认证、改造标准和激励机制方面采用共同的方法,不仅能提升当地建筑质量,还能实现跨境认可和投资。

– 用于社会公益的房地产投资信托基金(REITs)

新加坡的经验表明,房地产投资信托基金(REITs)如何为经济适用的绿色住房项目提供资金支持。中国可以扩大其房地产投资信托基金框架,以支持混合收入型、节能型住房开发项目,吸引机构投资者和个人投资者。

– 债务换可持续发展

通过将债务重组与可持续发展成果挂钩,开发商可以在获得财务喘息空间的同时,同时致力于绿色升级改造。这一创新融资模式可以在重点优先的城市更新区域进行试点。

How to Facilitate EU-China Collaboration

Close, stable and long-term connection between European and Chinese stakeholders is the cornerstone to overcome the key barriers to market entry and execution—be it regulatory understanding, technology transfer, pilot program design, or on-the-ground partnership development.

Then a well-established network of real estate developers, urban planners, technology providers, and green finance institutions can help:

o Match EU solution providers with real estate and construction needs in China

o Guide Chinese companies looking to adopt EU green building standards or enter the European market

o Coordinate joint demonstration projects based on smart construction and sustainable retrofitting

o Facilitate knowledge exchange on policy implementation and innovation

如何促进中欧合作

欧洲和中国的利益相关方之间紧密、稳定且长期的联系,是克服市场准入和执行过程中关键障碍的基石——无论是在对监管的理解、技术转让、试点项目设计,还是在实地的合作伙伴关系发展等方面。

一个成熟的由房地产开发商、城市规划师、技术供应商以及绿色金融机构组成的网络能够提供以下帮助:

o 将欧盟的解决方案供应商与中国房地产和建筑领域的需求相匹配;

o 为有意采用欧盟绿色建筑标准或进入欧洲市场的中国企业提供指导;

o 协调基于智能建造和可持续改造的联合示范项目;

o 推动在政策实施和创新方面的知识交流。

Closing Perspective: Building Tomorrow’s Cities Today

The challenges in China’s real estate sector are formidable, but so are the opportunities. With a focus on quality, sustainability, and international cooperation, the sector can reemerge stronger and more aligned with the country’s green development goals. The EU’s experience, governance policy, technology and standards—combined with China’s market scale and policy drive—can form a win-win path forward.

CNEUCN is committed to supporting this transformation by building platforms for dialogue, partnership, and action. The time is ripe to reimagine Chinese real estate—not just as a driver of GDP, but as a showcase of sustainable, resilient, and people-centric development.

As the sector transitions from its high-growth past to a more sustainable future, the winners will be those who:

– Embrace quality branding (not just square meters)

– Integrate smart, green technologies with verifiable certifications

– Create genuine community value through thoughtful placemaking

At CNEUCN, we’re seeing how strategic branding—when backed by real quality—can become a powerful stabilizer in volatile markets. Whether it’s through EU-inspired sustainable designs or tech-enhanced living concepts, the future belongs to developers who invest in meaningful differentiation.

结语:立足当下,建设未来城市

中国房地产行业面临的挑战十分艰巨,但机遇同样巨大。通过聚焦于质量、可持续性以及国际合作,该行业能够以更强的姿态重新崛起,并更好地契合国家的绿色发展目标。欧盟的经验、治理政策、技术以及标准,与中国的市场规模和政策驱动力相结合,能够开辟出一条双赢的前进道路。

仲欧脱碳科技(CNEUCN)致力于通过搭建对话、合作及行动平台来支持这一转型。如今,重新构想中国房地产的时机已然成熟——不应仅仅将其视为国内生产总值(GDP)的推动因素,而应将其看作是可持续、韧性且以人为本的发展典范。

随着房地产行业从过去的高速增长阶段向更具可持续性的未来转型,脱颖而出的将是那些做到以下几点的参与者:

– 注重品质品牌塑造(而不只是关注建筑面积)

– 将智能、绿色技术与可验证的认证相结合

– 通过精心的场所营造,创造真正的社区价值

在仲欧脱碳科技(CNEUCN),我们将看到,当有真正的品质作为品牌的支撑时,战略性的品牌塑造如何能够成为动荡市场中强大的稳定因素。无论是借鉴欧盟的可持续设计理念,还是采用科技赋能的居住概念,未来都属于那些致力于打造有意义差异化的开发商。